Copyright 2026 © swekartor. All Rights Reserved.

Information about Daily Pay Services

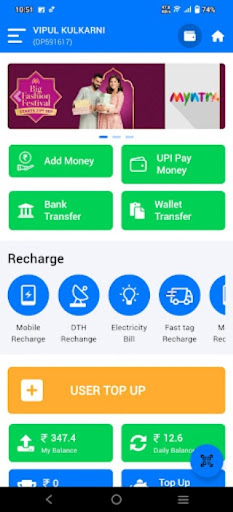

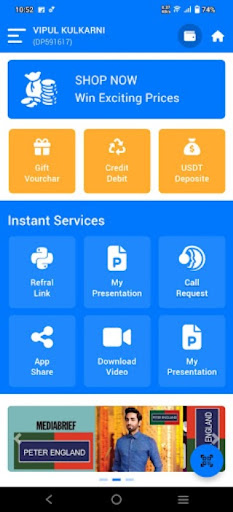

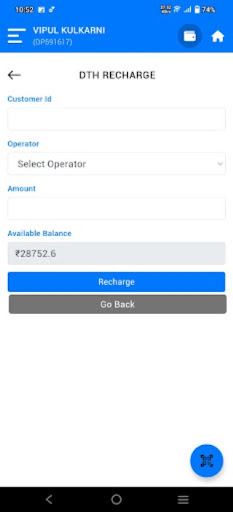

App Feature

Daily Pay Services aims to provide a simple hub for daily financial tasks such as recharges, UPI transfers, wallet transfers, gift vouchers, and basic money movement, wrapped in a user-friendly interface with an emphasis on secure processing.

Verdict

Verdict: A lightweight finance utility with promise, but its low adoption and lack of reviews make it a cautious try for now.

Who is it for

Best for:

- Users seeking a simple, free tool for basic payments and recharges

- Early adopters comfortable trying new finance apps with minimal footprint

Not ideal for:

- Users who need proven, widely trusted payment platforms with strong support

- Those requiring advanced finance features, integrations, or extensive rewards

Real-world User Experience

Users like it:

Insufficient public ratings/reviews to draw firm conclusions; the description highlights convenience, fast access to funds, and an easy interface.

Users complain about:

No reliable user feedback available; potential concerns include unclear regulatory/compliance details, minimal social proof (low installs, no rating), and vague scope of services.

Is it Worth Paying For?

The app is free with no ads and no in‑app purchases, so there’s no monetary risk. Given the lack of reviews, treat it as a cautious trial—avoid large transactions until you verify reliability.

How it Compares to Alternatives

Compared to established options in Finance (e.g., Google Pay, PhonePe, Paytm for UPI and recharges, or earned‑wage access apps with clear employer integrations), Daily Pay Services appears far less vetted: fewer installs, no ratings, and limited transparency. Larger alternatives typically offer verified merchant networks, customer support, dispute resolution, robust KYC, and proven security certifications. This app’s value would hinge on niche convenience or local features, which are not clearly demonstrated yet.

Summary

Daily Pay Services presents itself as a straightforward utility for recharges, UPI transfers, and wallet/gift‑voucher operations, emphasizing secure transactions and an easy interface. However, with no ratings or reviews and a small install base, it lacks the social proof and transparency typical of mature finance apps. If you try it, start with small, low‑risk transactions, verify UPI identifiers and beneficiary details carefully, and confirm support responsiveness. Users who need established protections, advanced features, or guaranteed interoperability will likely be better served by major payment apps until this service demonstrates more reliability and user feedback.

Ratings

Trending APP

Alternative to this app