Copyright 2026 © swekartor. All Rights Reserved.

App Feature

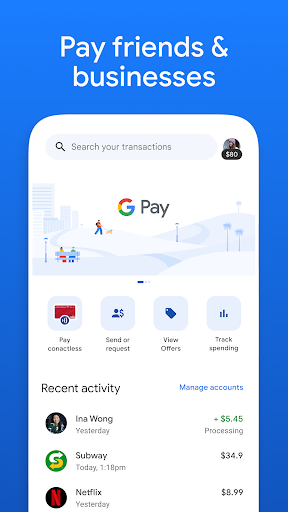

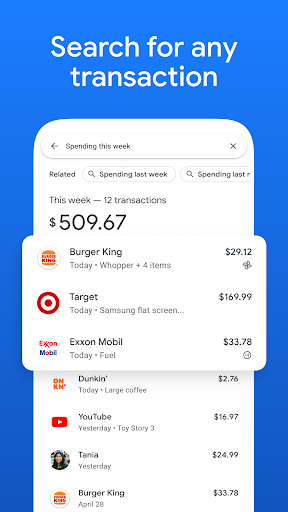

Google Pay enables quick, secure digital payments: send/receive money, pay merchants via tap/scan (region-dependent), split/group payments, check linked account balances, view expense insights, and autofill/pay on supported sites. It supports QR-based transfers, UPI flows in supported markets (e.g., India), and biometric/PIN verification. Note: the standalone U.S. app is no longer usable; tap-to-pay there shifts to Google Wallet.

Verdict

Verdict: A fast, feature-rich payments app for everyday transfers and bills, but U.S. users should move to Google Wallet and some reliability issues still surface for a subset of users.

Who is it for

Best for:

- Users in supported regions (e.g., India) who need quick UPI payments, bill pay, and QR scanning

- People who want a clean, secure app with transaction history and occasional rewards

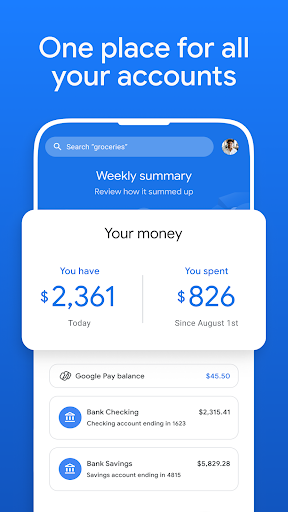

- Anyone managing multiple bank accounts and seeking simple balance checks

Not ideal for:

- U.S. users seeking a standalone app for tap-to-pay (use Google Wallet instead)

- Users who require advanced budgeting features like custom categories, spending limits, or robust analytics

- Those who need guaranteed refunds/support responsiveness during rare payment failures

Real-world User Experience

Users like it:

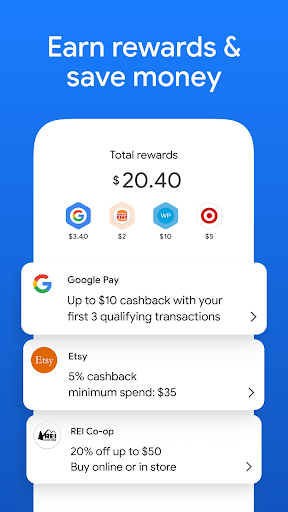

Smooth, fast, and secure payments; intuitive UI; instant transfers via UPI/QR; reliable bill payments; clear transaction history; occasional cashback/rewards; widely accepted by merchants.

Users complain about:

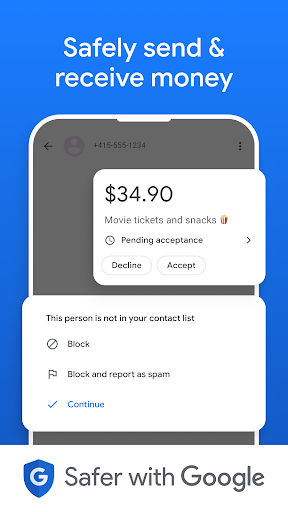

Intermittent glitches (payment stuck or delayed refunds), app logout during recharge for some, keyboard not appearing for manual transfers, restrictive screenshot policy for proofs/QR sharing, debit-card requirement for initial setup vs BHIM, and support responsiveness can be slow.

Is it Worth Paying For?

The app is free with no in-app purchases or ads; there is nothing to pay for. Value is excellent if you’re in a supported region.

How it Compares to Alternatives

Against PhonePe and Paytm (India), Google Pay offers a cleaner interface and strong security, but rivals may provide richer super-app features (recharges, commerce, mini-apps) and sometimes faster issue resolution. Compared to BHIM, GPay is more polished and merchant-friendly but may require a debit card for setup where BHIM can link directly. Versus Apple Pay/Samsung Pay (tap-to-pay wallets), GPay’s strength is P2P/UPI and QR ubiquity in supported markets; in the U.S., Google Wallet replaces GPay for NFC payments.

Summary

Google Pay is a polished, widely accepted digital payments app focused on fast, secure transfers, QR/NFC merchant payments, and simple money management. It excels at everyday UPI payments, bill pay, and keeping a tidy transaction history, with biometric/PIN protection and occasional rewards. Power users may miss deeper budgeting tools (labels, spending caps, custom categories), and a minority of users report reliability or support delays during failed transactions. Crucially, the standalone U.S. app is no longer usable—American users should switch to Google Wallet for tap-and-pay. If you’re in a supported market, GPay remains a dependable, user-friendly choice for daily digital payments.

Ratings

Trending APP

Alternative to this app