Copyright 2026 © swekartor. All Rights Reserved.

App Feature

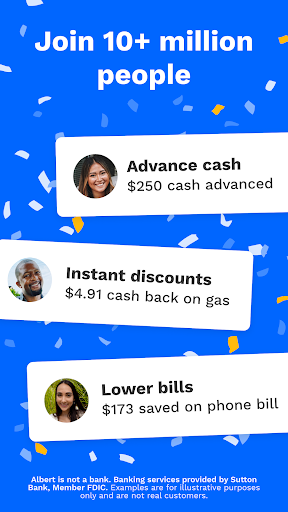

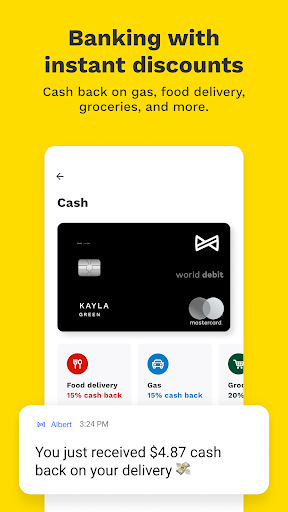

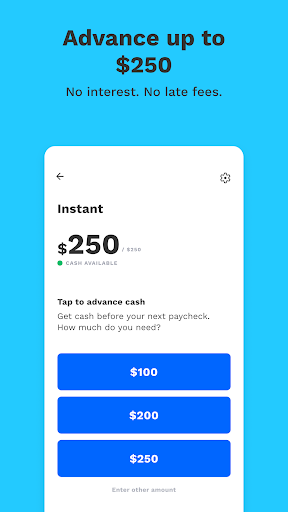

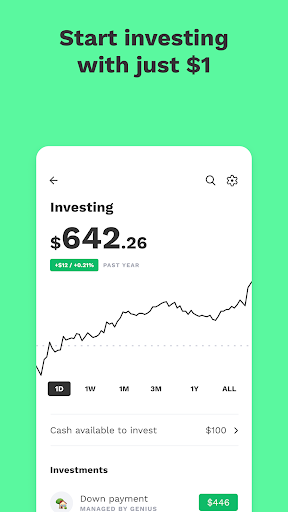

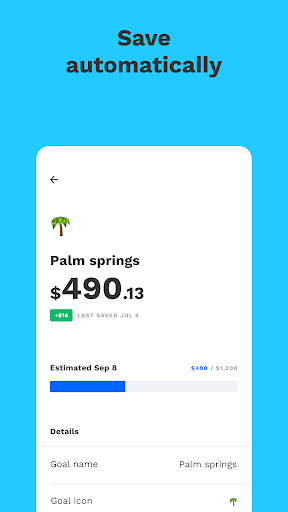

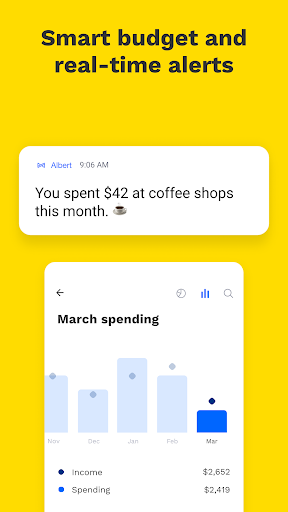

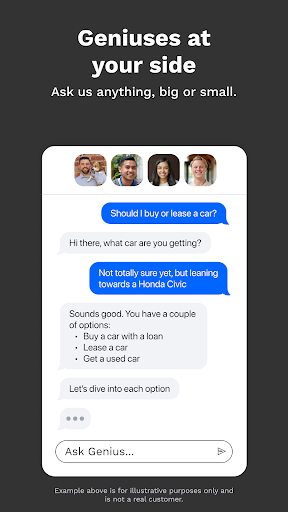

Albert is an all‑in‑one money app that combines budgeting, banking features (through partner banks), automated savings, cash back, early direct deposit, credit/identity monitoring, and investing (self‑directed and managed). Its AI-driven “Genius” analyzes spending to build budgets, find savings, and answer finance questions, while Smart Money automates transfers toward savings and investments. Albert is not a bank; services are provided via partner institutions with FDIC pass‑through coverage.

Verdict

Verdict: A capable all‑in‑one budgeting and cash‑management app with helpful automation, best if you’ll use multiple features but uneven eligibility and subscription costs won’t suit everyone.

Who is it for

Best for:

- People who want budgeting, saving, and basic investing in one app

- Users who benefit from small, automated savings and occasional cash advances

- Busy individuals who value proactive alerts, bill tracking, and 24/7 monitoring

Not ideal for:

- Those who need guaranteed, high cash‑advance limits or instant eligibility

- Users seeking advanced budgeting customization like envelope/zero‑based planning (e.g., YNAB)

- Fee‑averse users who won’t use Genius or High Yield Savings tied to the subscription

Real-world User Experience

Users like it:

Easy setup and intuitive design; effective automated savings that feel “invisible”; clear spending categorization and helpful summaries; timely bill/low‑balance alerts; quick resolutions from customer support; small cash advances that prevent overdrafts; gradual increase in advance limits with on‑time repayment; simple entry into investing.

Users complain about:

Inconsistent eligibility for advances (sudden ineligible status after repayment); relatively low advance limits for some; occasional delays in money movement reported by a subset of users; waiting period to qualify with new accounts; fees for instant transfers; frustration when account reviews take longer than promised.

Is it Worth Paying For?

Albert’s core pitch shines if you’ll actively use several premium perks: Genius insights/AI help, identity monitoring, and High Yield Savings (subscription required), priced at $14.99–$39.99/month after a 30‑day trial. If you mainly want occasional advances (subject to eligibility) or basic budgeting, the value may be harder to justify—especially given instant transfer fees and non‑guaranteed advance amounts. Power users who leverage savings APY, automation, and coaching get the best ROI; minimalists may prefer free or cheaper single‑purpose tools.

How it Compares to Alternatives

Compared to Dave, EarnIn, Brigit, and MoneyLion, Albert is broader: it blends budgeting, automated savings, investing, and monitoring with advances. Competitors often make cash advances simpler or more predictable but lack investing and deeper budgeting insights in one place. Against budgeting‑first apps (e.g., YNAB, EveryDollar), Albert is less granular but adds banking perks and automation. Versus Mint/Credit Karma Money, Albert’s automation and cash‑management feel more active, though subscription requirements and advance eligibility can be sticking points.

Summary

Albert: Banking on you combines budgeting, automated saving, cash back, early direct deposit, identity monitoring, and investing under one roof, guided by an AI assistant that learns your spending and nudges you toward better habits. Real users praise its ease of use, subtle but effective savings, practical alerts, and helpful support, with many relying on small advances to bridge gaps. The trade‑offs are uneven advance eligibility, sometimes modest limits, and a subscription that only pays off if you tap multiple premium features (e.g., Genius and High Yield Savings). If you want a single app to coordinate daily money tasks and light investing—and you’re comfortable with the subscription for the full experience—Albert is compelling. If you mainly need predictable advances or deep, rules‑based budgeting, specialized alternatives may fit better.

Ratings

Trending APP

Alternative to this app