Copyright 2026 © swekartor. All Rights Reserved.

App Feature

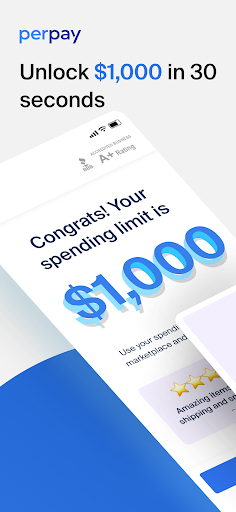

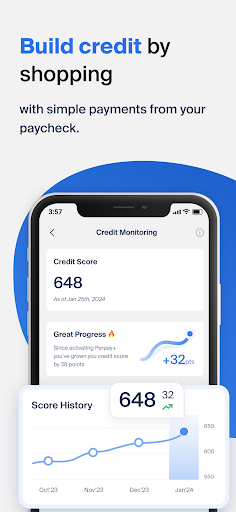

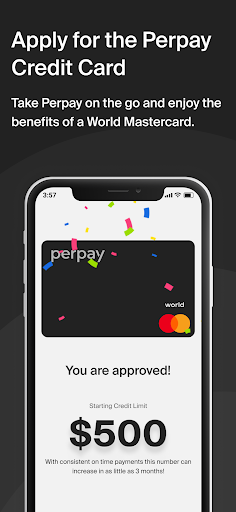

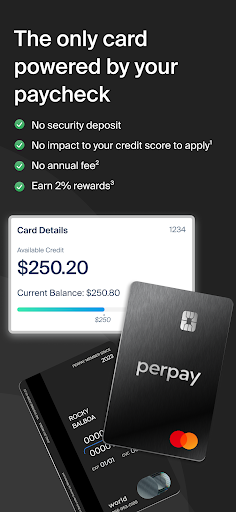

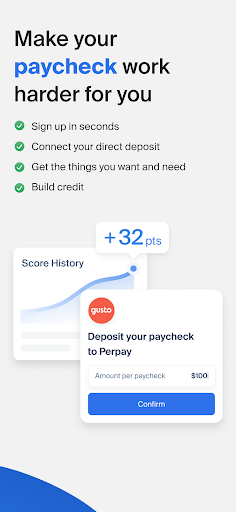

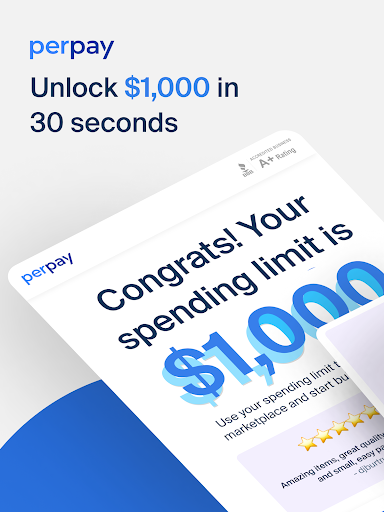

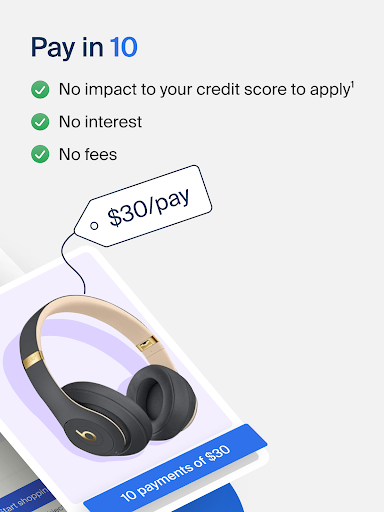

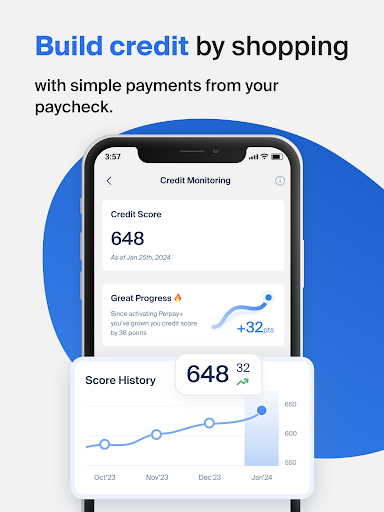

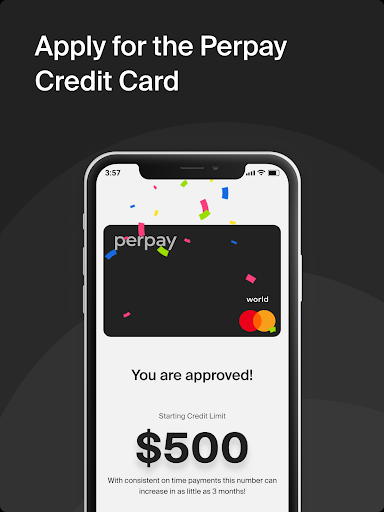

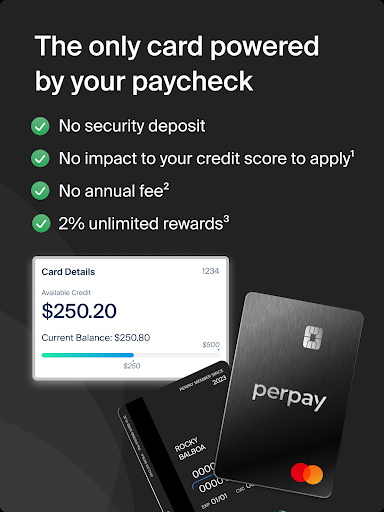

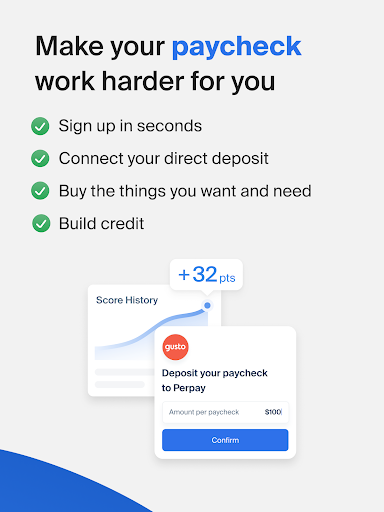

Perpay is a finance app and marketplace that lets you shop top brands with up to a $1,000 spending limit and repay automatically via paycheck deductions, with the option to report payment history to all three credit bureaus (Perpay+) to build credit. It also offers a Perpay Credit Card (up to $1,000 line, 2% rewards, no annual fee but $9 monthly servicing fee) with no hard credit check to apply.

Verdict

Verdict: A practical buy-now-pay-over-time option that helps build credit, but product markups and timing quirks won’t suit deal-seekers or impatient shoppers.

Who is it for

Best for:

- Shoppers with thin or damaged credit who want to build history while paying over time

- People comfortable with paycheck-linked, set-and-forget repayments

- Users prioritizing interest-free installments over getting the absolute lowest price

Not ideal for:

- Bargain hunters sensitive to retail markups versus standard store prices

- Users who need immediate shipping without waiting for an initial payroll deduction

- Those who prefer traditional credit products with broad limits and no servicing fees

Real-world User Experience

Users like it:

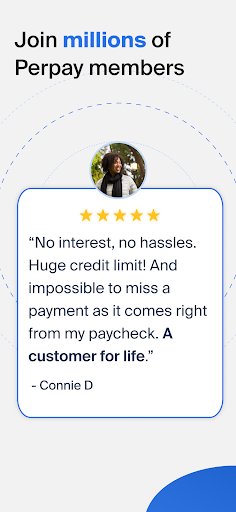

Easy, automated payments from paychecks; straightforward onboarding and navigation; wide product selection; tangible credit score improvements reported by users; responsive customer support that resolves hiccups; interest-free pay-over-time structure viewed as transparent and convenient.

Users complain about:

Some items carry noticeable markups; occasional app glitches and navigation quirks; shipping often waits until after the first payment; payment timing mismatches (e.g., semi-monthly schedules) and processing delays can cause confusion.

Is it Worth Paying For?

The app is free with no IAP. Costs show up as potential product markups on the marketplace and, for the credit card, a $9 monthly servicing fee (no annual fee). If you need structured repayment and credit building without interest or a hard credit pull, the value can outweigh the markup/fee; if you already qualify for low-APR cards or can pay upfront, cheaper alternatives likely exist.

How it Compares to Alternatives

Compared to BNPL apps like Afterpay, Klarna, or Affirm, Perpay’s standout is paycheck-linked repayments and optional reporting to all three bureaus, making it more explicitly credit-building. It’s less compelling for rock-bottom pricing than standard retailers or some BNPL deals. Versus secured credit cards, Perpay avoids deposits and can be easier to start, but has lower limits and, for the card, a servicing fee; secured cards may be cheaper long term if you qualify and manage them well.

Summary

Perpay blends a curated marketplace, paycheck-linked installments, and optional credit reporting to help users buy essentials and steadily build credit. Reviews praise its convenience, clear workflows, and supportive customer service, with many citing real credit-score gains. Trade-offs include higher-than-retail prices on some items, shipping after the first payment, occasional app hiccups, and a $9 monthly servicing fee on the credit card. If you’re rebuilding credit or prefer automated, interest-free repayments without a hard credit check, Perpay is a strong, low-friction option. If you prioritize the absolute lowest prices, instant fulfillment, or higher credit limits without fees, traditional retailers, BNPL competitors, or secured/prime credit cards may fit better.

Ratings

Trending APP

Alternative to this app