Copyright 2026 © swekartor. All Rights Reserved.

App Feature

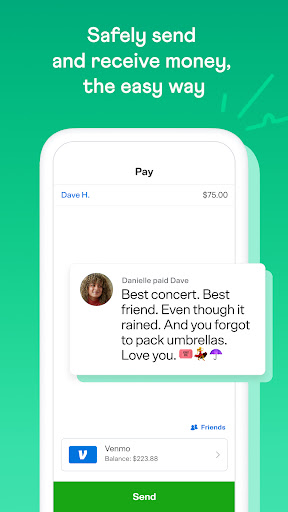

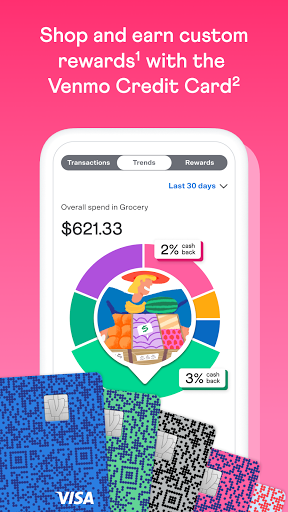

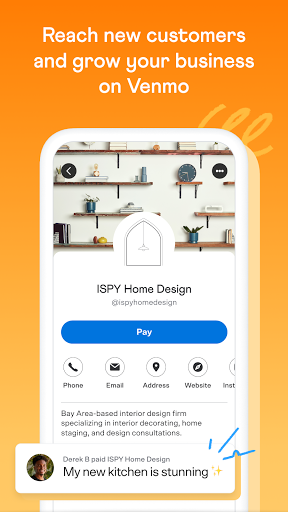

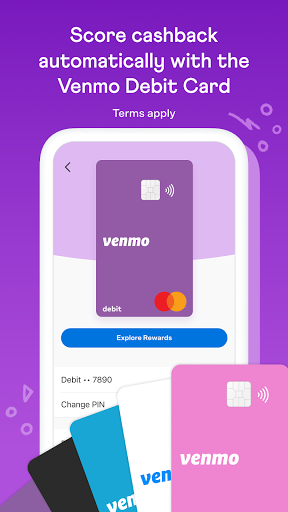

Venmo lets you quickly send, receive, and split payments with friends, add notes and emojis, and pay in-store or online via QR codes. It also offers a debit card, a cash‑back credit card, basic business profiles, teen accounts, optional direct deposit and instant transfer, and the ability to buy/sell crypto within the app.

Verdict

Verdict: A fast, social peer‑to‑peer payments app with broad extras, best for everyday splits and casual transfers, but not ideal if you want bank‑grade simplicity or high limits.

Who is it for

Best for:

- Friends and families splitting bills, rent, or group expenses

- Users who want social features, QR payments, and instant P2P transfers

Not ideal for:

- People who need very high transfer limits or strictly bank‑style simplicity

- Privacy‑first users who dislike social feeds or want minimal data visibility

Real-world User Experience

Users like it:

Fast and reliable person‑to‑person payments; easy requests and reminders to avoid awkward payback conversations; useful group split feature; smooth bank transfers (standard free, instant available); card perks and occasional cash back; overall intuitive interface and steady feature growth.

Users complain about:

Occasional bugs (e.g., error messages, missing transaction views); risk of paying the wrong person without double‑checking; security concerns if phone is unlocked without a PIN/App lock; group split UI can be confusing; transfer limits and balance handling can be restrictive.

Is it Worth Paying For?

The app is free with no in‑app purchases; standard bank transfers are free. Expect optional fees for instant transfers and certain card/transaction types. For typical use—splitting, casual payments, standard transfers—there’s strong value at no cost.

How it Compares to Alternatives

Compared to Cash App, Venmo leans more social and offers broader splitting and feed features, plus both debit and credit card options; Cash App can feel simpler and more direct. Versus Zelle, Venmo is more consumer‑friendly for casual splits and requests, while Zelle is more bank‑integrated and straightforward (but lacks social feed and extras). Against PayPal, Venmo is lighter and faster for domestic P2P among friends; PayPal retains stronger international and merchant tools but with more friction for casual splits.

Summary

Venmo is a popular, social‑first payments app built for quick splits, IOUs, and everyday transfers. Beyond basic P2P, it supports QR checkout, a debit card for everyday spending, a cash‑back credit card, teen accounts, business profiles for side gigs, and optional direct deposit/instant transfer. Users praise its speed, reminders, and overall ease—though some report intermittent bugs, confusing group splits, and the risk of misdirected payments without careful confirmation. Privacy‑minded users can keep payments private, but the social feed may still not appeal to everyone. With free standard transfers and optional paid conveniences, Venmo offers strong value for casual and social payments, while power users needing high limits or bank‑centric simplicity may prefer alternatives.

Ratings

Trending APP

Alternative to this app