Copyright 2026 © swekartor. All Rights Reserved.

App Feature

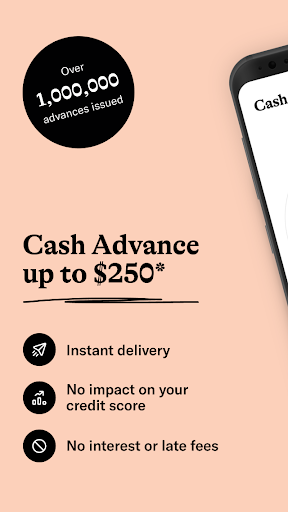

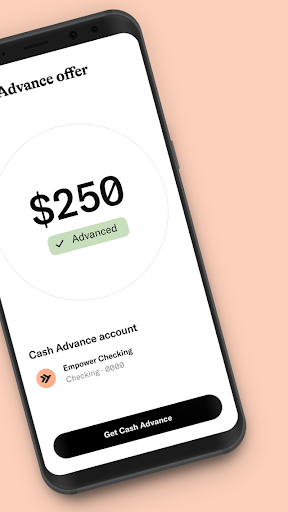

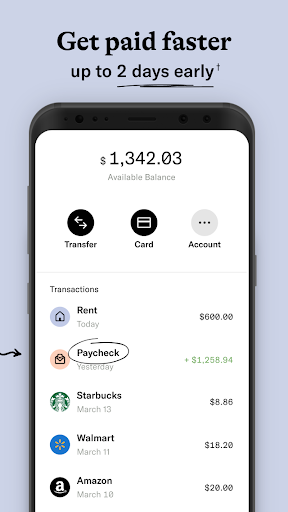

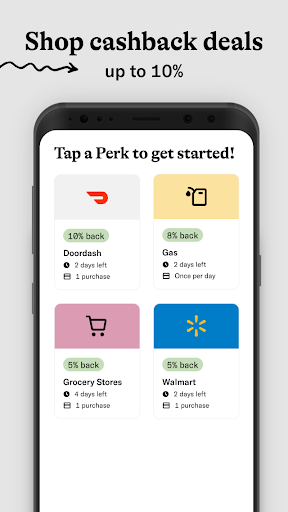

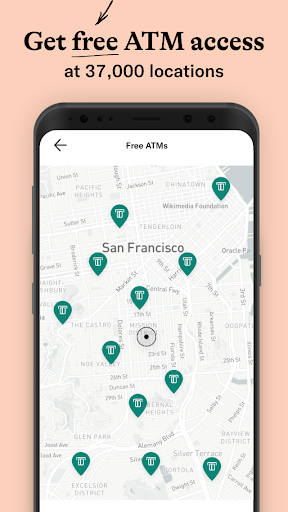

Tilt provides short-term cash advances (up to ~$400) with no credit checks, optional instant delivery (fees may apply), and no interest/late fees, plus access to a bank-issued credit card (no security deposit, reports to bureaus), a line of credit (up to ~$1,000 with growth via on-time payments), credit score monitoring, budgeting alerts, and automatic savings. It requires linking a bank, uses real-time income/spend to evaluate eligibility, and runs on a $8/month subscription after a 14-day trial.

Verdict

Verdict: A strong, flexible cash-and-credit toolkit for short-term gaps and credit building, but the subscription and variable limits mean it’s best used intentionally, not habitually.

Who is it for

Best for:

- People who need occasional, fast cash with transparent fees and no interest

- Users building or rebuilding credit who want reporting and gradual limit increases

- Budgeters who value in-app score monitoring, alerts, and autosave

Not ideal for:

- Anyone seeking large, long-term financing or lowest-cost traditional credit

- Users who dislike monthly subscriptions or linking their bank

- People depending on advances every pay cycle without a clear repayment plan

Real-world User Experience

Users like it:

Fast approvals and funding (often instant to debit), clear pricing with no interest, flexible payback date options, limits that can increase with on-time repayment, and overall better value than payday lenders. Many note smooth setup and that fees for instant delivery are relatively low and paid at repayment.

Users complain about:

Monthly subscription can surprise new users if they don’t cancel when not borrowing; initial limits may start low for some; instant delivery has a small fee; not a long-term solution for ongoing cash shortfalls.

Is it Worth Paying For?

If you use it occasionally to bridge short-term gaps, the $8/month subscription plus optional instant fee can be cheaper and clearer than payday loan interest and overdraft penalties. If you rarely borrow, cancel after the trial or months you don’t need it to avoid paying for unused access.

How it Compares to Alternatives

Compared with Dave, EarnIn, and Brigit, Tilt emphasizes a mix of cash advances, a WebBank-issued credit card, and a FinWise line of credit with reporting—useful for building credit over time. Users report higher initial limits and more flexible repayment date choices than some competitors, while pricing remains subscription-based with optional instant fees similar to peers. Unlike overdraft-style options (e.g., SpotMe), Tilt evaluates real-time income/spend and can grow limits with on-time payments.

Summary

Tilt (formerly Empower) aims to make cash and credit more accessible by assessing real-time income and spending rather than relying solely on traditional scores. For short-term cash needs, it provides no-interest advances with optional instant delivery, plus a credit card and a line of credit that report to bureaus and can scale as you pay on time. Add-on tools—autosave, budgeting alerts, and score monitoring—help reduce repeat borrowing. The trade-offs: an $8/month subscription after a 14‑day trial and small instant delivery fees, with initial limits that may start modestly. If you need occasional, fast, transparent financing and want pathways to build credit, Tilt is compelling. If you rarely borrow, dislike subscriptions, or need long-term financing, traditional credit products may fit better.

Ratings

Trending APP

Alternative to this app